Automated Claims Processing – Why is it important for the insurers?

Is the insurance claim process becoming overwhelming due to lengthy processing times? Automated claims processing can alleviate this burden and revolutionize your claims processing procedures.

Insurance companies have diligently worked on automating various claims management phases over the years. Some insurers have witnessed remarkable improvements in performance and productivity by incorporating technologies such as chatbots and modernizing claims platforms. Beyond cost savings, artificial intelligence, and document ingestion capabilities expedite insurance claims processing.

One of the core responsibilities of insurance companies is collecting information about an incident, including details like the policyholder’s name, policy number, address, and the time and date of the event. Embracing an automated claims processing system not only leads to cost efficiencies but also ensures enhanced accuracy and efficiency in handling claims.

How does Automated Claims Processing Work?

When an insured person meets with an accident and submits an insurance claim, it undergoes a comprehensive inspection process to ensure compliance with all regulations. Therefore, automating the processing of insurance claims is primarily an issue of speed and error-free performance for insurers. The benefits of automation are manifold, as it not only expedites the claim evaluation procedure but also enables the identification of fraudulent claim-related activity.

Here are the steps to automate the claims processing:

- The initial process starts when a policyholder notifies the insurer of a claim. This can frequently be accomplished using a smartphone app or website. The policyholder submits basic information related to the claim, including the incident’s date, location, and any supporting records or photos.

- After a claim is filed, the insurer evaluates it using automated technologies to see if it falls inside the policy’s coverage. The claims management services involves reviewing the alleged damages, evaluating the policy terms, and contacting third-party databases to confirm the claimant’s identity and track record of previous claims.

- When the insurer determines the claim is legitimate, it will start the validation process by obtaining further data, such as repair estimates or medical records. This process can also be automated, with software gathering information from multiple sources and evaluating the allegation’s veracity using AI algorithms.

- The insurer will decide on the claim based on the data acquired throughout the evaluation and validation phases. The system can also automatically determine the proper payment amount or coverage level using pre-established rules.

- The insurer will start paying the claimant once the claim is accepted. This involves using electronic funds transfers or other digital payment options to automate the payment procedure.

- Lastly, leverage automated technologies to evaluate the claims data to find patterns and trends that may enhance the claims process and lower fraud.

What are the top insurance claims automation trends?

The insurance sector has seen a radical move toward automation in recent years, especially when it comes to claims processing. Artificial Intelligence (AI), Intelligent Process Automation (IPA), and Robotic Process Automation (RPA) are the three major trends in claims insurance automation dominating the industry.

Artificial Intelligence

Insurers can analyze immense volumes of data using machine learning techniques and evolved algorithms. Research reports indicates that these innovations can result in significant time and cost savings, reducing the costs associated with claims regulation by 20–30%, processing costs by 50–65%, and processing duration by 50–90%, all while improving the caliber of customer service interactions.

Intelligent Process Automation (IPA)

IPA creates a more comprehensive and flexible automation method by fusing AI and RPA. Apart from routine tasks, it acquires knowledge and makes well-informed decisions using real-time insights and previous data. However, insurers can streamline claims operations by automating complex procedures. They can use data to make better decisions.

According to multiple cases reported by McKinsey Digital, IPA has been successfully adopted by businesses in various industries. They’ve found that up to 70% of current tasks might be addressed by automation. This change has resulted in continuous cost savings of 20% to 35%. Furthermore, it has resulted in an incredible 50% to 60% decrease in straight-through process time. As such, these businesses often see a return on investment (ROI) in the triple digits.

Robotic Process Automation (RPA)

RPA uses software robots, sometimes known as “bots,” to automate repetitive operations in claims processing. They extract data from multiple sources, validate claim information quickly, and update system records. It reduces human error and frees employees to work on more complex tasks. According to McKinsey case studies, the ROI of RPA implementation in the financial services industry can improve by up to 200% in the first year.

How Automated Claims Processing can Benefit Insurers?

With modern claims solutions, insurers can automate claims process and stay ahead in the market. Let’s dive into its benefits:

Enhanced Efficiency:

Automation speeds up and simplifies the claims process while reducing the amount of manual work.

Increased Accuracy:

Automation increases accuracy in claims processing by lowering the chance of human error.

Faster Turnaround Times:

When you process insurance claims, it ultimately improves the turnaround time of settling claims.

Improved Customer Service:

You can enhance customer service by processing claims quickly, processing accurately, and responding to consumer inquiries in minutes.

Decreased expenses:

Automation lowers the demand for manual labor, which can boost profitability and cut costs.

Enhanced Compliance:

Automation lowers the possibility of fines and penalties and helps guarantee compliance with regulatory regulations.

Final Thoughts

Claims happen, even if neither clients nor insurers like to see them happen. Clients, therefore, want their problems settled swiftly and amicably, while insurers seek accuracy, economy, and zero fraud. Automated claims processing in the insurance industry is available to help make the process seamless.

Regarding market demand, insurance companies have a pressing need to automate the processing of their claims. In the next years, those who ignore automated claims processing might not make it because their competitors’ administrative costs will be far lower.

If you are looking for reliable claims management services, ISW have got you covered. Get in touch with our experts at: info@insurancesupportworld.com or +1 646-688-2821.

[ctashortcodebutton]

How can Insurers Stay Relevant in an Era of Disruption?

We all are aware of the disruption the insurance industry is experiencing especially from all sides. A significant challenge of adapting to the new normal has come up after the COVID-19 outbreak, and insurers need to find more ways to deal with it. Besides, the growing competition in the market (that was already there before the pandemic) increases the difficulty of thriving in today’s demanding market. Above all, they have to deal with the changing demands and expectations of the customers.

Several questions have been unanswered in the previous months; however, let’s read what industry experts say about how insurers can stay relevant in an era of disruption.

1. Adapt to the Evolving Digital Landscape

John Holloway, Co-founder of NoExam

Traditional insurance companies will need to look to partner with or invest in new startups that aim to disrupt the market. We have already seen this happen to an extent, but we have yet to see a new company really disrupt the insurance market in a wide-spread way.

Insurance companies have the capital, but they will need to stomach a bit more risk on their balance sheets in the form of partnerships and investments if they want to stay relevant. Disruption is coming; it is just a matter of when.

At a minimum, insurance companies need to invest in the digital experience from mobile apps to easy to use websites to streamlined digital communications. Consumers have reached a point where they will not tolerate frustrating online shopping experiences. The time has long since passed to adapt to the evolving digital landscape.

2. Embrace Technology

Tal Shelef, Realtor and Co-Founder of Condo Wizard

Insurers should embrace technology when aiming to stay relevant in these harsh times. Reach out to customers and maintain relationships through digital campaigns. Aim to provide the information they would find useful and relevant to help keep their interest. By doing so, insurers are not only showing customers that they care, but they are also distributing necessary knowledge and actions needed to help beat out the pandemic.

3. Utilize Data and Have a Customer-Centric Approach

Adrian Mak, CEO of AdvisorSmith , AdvisorSmith

Digital disruption affects insurers in two major ways:

1) Risk analysis and pricing

2) Customer acquisition

For risk analysis, increasing amounts of digital data generated by smart devices can improve the quality of insurers’ underwriting models and allow them to offer more accurate pricing. Think of sensors that measure how aggressively a driver accelerates, or satellite photos and machine learning that allows insurers to see if properties are accurately described.

For customer acquisition, the big opportunity for insurers is to invest in systems that allow customers to get quotes in real-time and purchase directly. The disruption here can come from new upstarts who are digital-first and have built tools to allow instant quoting, underwriting, and purchase.

Also Read: Remote Working & Insurance! Can they Go Hand-in-Hand?

4. Update the Buying & Underwriting Process

Sa El, Co-Founder of Simply Insurance Simply Insurance

To stay relevant, insurance companies are going to need to update both their buying process and underwriting process to an online platform that is super simple and fast to use.

If you look at the generation of people who are currently buying insurance and the ones that are going to need it in the future. It’s easy to see that people want things fast and want to be able to do it online.

5. Adopt Technological Advancements

Stacey Giulianti, Chief Legal Officer, Florida Peninsula Ins Co

I’m not convinced that insurance ‘disrupters’ are anything more than just better marketers. Insurance is still a business of collecting the proper premium, servicing the customer, and accurately managing your underwriting results. Apps on a smartphone won’t change the fundamental business of property insurance. Carriers should, however, adopt technological advancements that help the customer manage their policy and utilize their benefits.

6. Key Adoptions for a Successful Future

Rogan Dwyer, Chairman of Observatory Strategic Management

The insurance industry is, or shortly will be, technically bankrupt through its own refusal to move with the times. Carriers have failed to change the business model or perception of what an insurance company is in the modern world. By failing to clarify insurance coverage, failing to shoulder their responsibilities to place the interests of their customers first (the policyholders), and failing to embrace new technologies that reduce costs, redundancy, and risk, they will be forced to turn to governments for bailouts.

If we equate such bailout to Lloyd’s own Recovery and Restoration sleight of hand of the mid-1990s, the blueprint is there for an unencumbered insurance market to rise Phoenix-like to provide the services and support individuals’ and businesses’ need for the future. This successful future, therefore, relies upon the following adoptions:

- Policyholders primacy – carriers HAVE to recognize that they don’t exist without clients.

- Risk mitigation becomes a partnership with policyholders so that interests are aligned – technology incubators are critical to this.

- Costs and processes are streamlined and innovation companies embraced – again, third party system innovators must be involved.

- Agents are recognized as agents of the policyholder and not held to ransom by carrier appointments and contingent commissions .

- Cash flow is recognized as a fundamental underpinning of industry, and more must be done to safeguard and facilitate that aspect. Simplify the insurance contracts to speed up payment and remove attorney costs from the policyholders.

Insurers will always be relevant and are the DNA of the business, but a successful insurance company must focus on looking forward rather than back. Actuaries should no longer be the driving force for rating and coverage. Transfer of risk to the appropriate vehicle must take over.

7. Digital Technologies could Help Insurers Stay Relevant

Justin Nabity, Founder, and CEO at Physician’s Thrive

Insurers are facing disruptions from every side. They have to meet customer expectations as well as compete with digital-first companies. The industry is changing due to the rise of technology, and the change is genuine because these new technologies are modifying the businesses, and disruptors are emerging. The ignorance in acknowledging the challenges that came with technology, plus failure to identify and avail of the opportunities, was a big mistake. This was expected because the performance of insurers was very weak, i.e., average top-line growth sales slowed, and the rate of net assets also decreased in the past two years.

Analyzing the current state of the market, insurers must find ways on how digital technologies could help them stay relevant. Many researchers estimate that digital trends in the market are set to create massive value in the coming years. Therefore, insurers need to embrace new technology to avoid the risk of losing a competitive edge. Insurers can take advantage of the explosion of data because of the internet, coupled with machine learning. This will not only help them in making their monetization policies better but also aid them in providing the most optimal value to their customers.

8. Invest in Digitization & Data to Thrive

Jacob Sheridan, CEO & Co-Founder of TPA Stream

One of the promises of digitization is unprecedented access to data. From claims data to enrollment data, as well as pricing, usage, and actuarial data, the amount of information insurers can leverage is exponentially growing. This data unlocks different ways to think about insurance, allowing providers and employers to more easily build custom plans at competitive prices, all at scale. Forward-thinking insurers will need to make investments in digitization and data to thrive in a landscape that is becoming more competitive each year.

9. Consider AI-Driven Claims Management

Dan Roselli, Managing Director of RevTech Labs

The rapid acceleration of AI-driven claims adjustment is being fueled even more now due to COVID-19 and the idea that in this environment, ‘remote is better.’ AI is allowing quicker and more accurate claims management that will dramatically reduce fraud and costs for the insurers. It seems like every one of our Insurance partners is focused on this hotspot now.

Conclusion:

In order to stay relevant in the era of disruption, insurers first need to have a clear and strong understanding of the disruption itself. Then only they can respond effectively to today’s evolving digital landscape. Consequently, they will recognise the need for product and service development to match customer demand and market trends.

Apart from focusing on the digital transformation of processes, insurers need to improve their traditional operational policies and build new, customer-centric strategies.

Amid handling all of this, insurers may experience heavy loads of work; moreover, the pandemic has increased the workflow intensity. In such circumstances, they might want to consider outsourcing claims management services to reduce a considerable portion of the burden. At Insurance Support World, we understand the pressure insurance carriers and agencies are bearing and offer them our quality back-office support. We have been providing insurance back-office outsourcing services to clients across the globe since 2008. Call us at +1 646 688 2821 or send an email at info@insurancesupportworld.com.

Recommended Posts:

Practices to Improve Client Retention in Your Insurance Agency

[ctashortcodebutton]

How Insurers Handling Claims Challenges with Modern Solutions?

The insurance claims process in today’s modern business era is becoming complex. With a lot of data continuously becoming crucial, carriers need to settle claims appropriately while determining potential frauds without taking much time. Apart from technological challenges, insurance carriers and agencies must deal with customers better during stressful times. Now is the perfect time to create a balance between automation and empathy in order to provide customers with the experience they have always been looking for. That’s where modern claims solutions come into play.

The road to success is no longer easy, and insurers need to tackle big walls of difficulties that come their way. This writing piece will present challenges concerning claim management and how insurers are dealing with the same.

Handling Claims Challenges the Right Way

Navigate and conquer claims challenges with effective strategies and solutions that ensure the right path to resolution.

1. The Need for a Systematic Overhaul

With the involvement of decision-makers and company stakeholders, insurance claims management services process includes a variety of business rules and regulations, making it a complicated process to execute. As a result, employees’ responsibilities increase, and customer experience gets affected.

Insurers looking to automate these functions will need to manage and keep track of numerous activities and have strategies, policies, and comprehensive systems to efficiently handle the entire process.

2. Increasing Customer Expectations

Apart from their insurance needs, customer experiences (buying and servicing) generally impact what they expect from insurance providers; as a result, customers’ expectations are growing. Insureds claim for compensation once in a few years; thus, carriers can ensure they handle customers’ emotions as per the severity of the situation while managing to process the claim requested quickly.

The complexity involved in the process can be reduced with the help of advanced, latest technological tools. However, for clearing doubts that customers have and building the trust factor, human intelligence is vital and can never be replaced.

3. Increasing Variety of Emerging Technologies

Carriers are now evaluating new players in the insurtech landscape and finding the best possible ways they can invest in solutions provided by them in order to lower claim processing complications and streamline workflows. More and more insurance technology providers are increasingly focusing on making improvements in the claims process and delivering modern claims solutions.

This enables insurers to enhance customer engagement and operational efficiencies dramatically.

Here, the real challenge is not utilizing technology but determining what tech-solutions would bring the desired results and the appropriate implementation of the same in their current claims process.

4. The Requirement for Skilled Employees

Insurers are experiencing a workforce shortage; it is getting difficult to attract new talent, adding to their loss as their skilled employees retire. As a response to these challenges, many are automating basic, repetitive functions that require no special skills and training their existing staff to create a workforce they can leverage in this digital era. Many core insurance processes still run on coding languages, and it is becoming hard to recruit individuals having excellent coding skills.

Insurance companies looking to grow in the current time need to consider software solutions they can use to capture more portion of the market and increase profitability. For instance, their business analysts can use data and some analytical tools to determine market demand, expectations, changes, etc. to modify insurance products, service delivery, operations, and much more.

5. The Challenge of Shifting from Legacy to Modern Claims Systems

Many carriers are dealing with bottlenecks caused by extensive resource utilization in maintaining legacy systems. They rely on systems that are not very flexible, which often leads to delay in streamlining operations and fulfilling customer requirements. All of this limits their ability to respond to changes in market and customer behaviour effectively. Even if they want to shift to modern systems, there are phases where they need to develop and test new methods, causing delayed innovation and progress.

Today’s insurers need to replace legacy systems with modern claims solutions to prevent all possible repercussions of their dependence on outdated technology, processes, etc. Although this shift (especially a successful one) may take several years, the global investments in AI and insurtech indicate that insurers cannot avoid the modernisation of legacy systems.

Technological trends in the insurance industry are growing rapidly that the insurers considering claim system transformation are already lagging behind their competitors. The long lasting impact of this transformation can result in enhanced capabilities, improved claim management, informed decision-making and better overall outcomes.

Now is the Time to Prepare for a Better Future

As customer expectations are changing in the digital age, Insurers need to ensure that they change the way they process claims – the entire claim management system. In order to meet customer demand, insurers need to serve them round-the-clock and enable customers to choose whether they want to communicate with support executives or get help from virtual assistants. Having an easy, transparent process to deliver what customers deserve can dramatically enhance customer experience and loyalty.

As an insurance business owner, you need to become a part of digital ecosystems that many established insurance companies have built to solve issues customers face and improve their claims journey by coming together in the demanding insurance market. You need to have a customer-centric approach to attract potential customers and retain the existing ones in the long run.

You may increase the premium to solve half of the problem caused by growing numbers of claims, but this will eventually result in higher customer expectations; they will seek excellent insurance products and services. Digitizing some of the insurance processes can help reduce operational costs and improve customer service, leading to higher customer satisfaction.

Conclusion

Modern claims solutions empower insurers to improve their operational efficiency and performance and simultaneously enhance customer engagement and interaction. Besides insurtech, the utilization of data and some analytical tools can help make continuous improvements in the entire process.

With automation and AI, you can prioritize customers and handle their expectations effectively; this will include guiding customers to choose the most suitable insurance products and connecting them with internal systems, encouraging them to use self-service portals.

You need to identify market trends, opportunities, compliance requirements, red flags, and operational inconsistencies in order to establish a new, improved system for the claims process. Consider leveraging technology to bring innovation in your insurance business, which can also bring agility to your organisation.

For the successful execution of your plans, strategies, and methods, you may need to collaborate with firms that can help you tackle all the challenges discussed above. At Insurance Support World, we have a dedicated team of insurance professionals ready to serve you with the best insurance back-office services. We have been delivering quality insurance process outsourcing services to clients since 2008 and assure you that you will receive the same. To know more about our comprehensive range of solutions, call us at +1 646-688-2821 Or email at info@insurancesupportworld.com.

[ctashortcodebutton]

COVID-19 & The Insurance Industry! What are the Biggest Challenges?

Coronavirus is a massive challenge to humanity that is not only making things complicated for human sustenance but also the worldwide economy. The insurance industry is one industry that has been impacted the most by COVID-19 and let us know from some industry experts as to what all challenges they are facing presently.

1. Dealing with a Bulk of Customer Calls

Alexis Feinberg, Senior Account Executive | Matter Communications

One challenge you may want to consider for your story is that right now, insurance companies are being hit with a surge in customer calls-from issues surrounding healthcare bills to concerns about auto payments. The number is staggering: hold times during COVID-19 have ballooned by as much as 38%. Dealing with longer hold times means more frustrated (and often angry) customers. So how can insurance companies balance handling huge numbers of customer inquiries while keeping customers happy?

The answer lies in the right combination of training and technology. More specifically, insurance companies should be strategic about training and which technology they select because:

- A well-trained representative is much more valuable-they personalize the customer experience, which will resolve issues faster and with better customer satisfaction

- AI-based technology can help automate simple tasks, which allows representatives to spend the bulk of their time helping customers

This game-changing combination will ultimately help with the volume of customer calls while giving representatives the support they need.

2. Medical Underwriting has become a lot Complicated

Heidi Mertlich | No Physical Term Life

Due to stay-at-home mandates most states have in place to varying degrees, medical underwriting has become difficult, in not impossible in many cases. As a result, life insurance applications have been delayed. Some carriers

are turning towards no exam life insurance underwriting.

Several carriers have severely restricted the ages of potential applicants. For instance, a large number of life insurers won’t even accept life applications for clients over the age of 70. Furthermore, your application may also not be accepted if you’re 60 or older with certain health conditions.

There are still a few carriers that will write policies on these people, however, it certainly limits the universe of carriers that an independent agency would normally have access to.

3. Not Investing in Enrollment Technology

Adam Hyers, President at Hyers and Associates, Inc.

There are several challenges to our industry right now. One is that many insurance carriers are behind in rolling out enrollment technology. So, many insurance transactions have been face-to-face through the years that many companies did not invest in this technology. Now that we can’t meet with our clients, it’s difficult to finalize some insurance purchases. Mailing mounds of paperwork back and forth for a life or annuity policy is not easy for some consumers. And many don’t want to visit the post office.

On the group health insurance side, there are many smaller companies that have temporarily shut down. They are trying to keep their employees on payroll while also maintaining their health insurance coverage, but that’s even difficult for some. The last thing they want to do is to drop a plan and then try to reconstitute it later. Many of the insurance companies are deferring premiums, but it’s been difficult to work through this on the fly.

4. Prior-Authorization Request Elimination is making Customers Irritated

Dan Moyer, VP of Sales and Marketing at RA Fischer Co.

Our healthcare system is currently overwhelmed. In response to the influx of new claims, insurance companies have altered their normal workflows in order to expedite processing. Many no longer require prior-authorization requests. While, in theory, this eliminates a step toward getting medical equipment covered for a patient, if you’re an out-of-network company or you bill under a miscellaneous code, we’ve seen claims that normally would’ve been approved get denied over the last two months. Why? Insurance companies still largely rely on outsourced customer service call centers and representatives who have limited access or decision making power during the claims process.

Previously, a prior-authorization request from an out-of-network company could’ve been supplemented by a gap except for a request. By providing insurance companies with supporting evidence – from a medical letter of necessity to the doctor’s chart notes – we’ve traditionally been able to get our durable medical equipment covered for patients. However, with the elimination of the prior-authorization step, insurance companies are immediately (almost automatically) denying out-of-network or miscellaneous claims. This has obviously been frustrating for patients who are counting on their insurance to cover their medical supplies and services.

5. Insurers are Struggling with the Adoption of Technology

Shawn Plummer | The Annuity Expert

From my perspective, agents are not sure how to conduct their business virtually in an efficient manner. I see them starting from scratch in terms of marketing, communication, and processing new business electronically.

They’re going from paper applications and dinner seminars to figuring out to market virtually via the internet or digital marketing. I see insurance companies scrambling to figure out how agents and advisors should market themselves in a compliant way, and process new business virtually at the same time.

My recommendation for insurance companies is to develop agent-assigned affiliate landing pages or portals that they can send to their clients to fill out applications directly. Some insurance industries have adopted this method, while others are slow to catch up.

6. No Sharing of Space with Roofing Contractors

Jonathan Abramson | Metro City Roofing Denver

Our sales professionals typically meet with insurance adjusters at a customer’s property and are on a roof together during the insurance adjuster’s inspection. Once an insurance claim is approved, we work to settle each insurance claim with a supplement process.

Since COVID-19, insurance companies have established new processes where they cannot meet with roofing contractors on a roof together. Depending on the insurance company, policy prohibits a contractor to be present, share the same ladder. We had one insurance adjuster in Loveland who required the homeowner to be out of the house 1 hour ahead of the inspection so no recent air breathed could escape through a vent while the adjuster was on the roof.

On another recent Denver insurance claim, we were asked to arrive 1 hour ahead of the insurance inspection and mark the roof with sidewalk chalk, so when the adjuster arrives, she could immediately see where we believe there is hail damage. Once we’ve marked the roof, we needed to get off the roof, remove our ladder, and wait in the car.

7. Increased Claims leading to Financial Disruptions

Anna Barker, Logical Dollar

One of the biggest challenges facing the insurance industry at the moment is *in relation to their liquidity*. Much like companies in most other industries, these are particularly challenging times from a financial perspective.

Unlike other companies, however, *this isn’t an issue that insurance companies have historically had to face in light of their business model* of receiving premiums upfront and being able to invest these funds in preparation for any payouts.

*The dip in the market also coincides with a significant increase in claims*, including medical, life insurance and, where applicable, business interruption claims. *This further contributes to issues of financial viability*.

*Insurers will thus have to take similar financial steps that other companies are now facing*, including canceling dividend payouts and reducing operating costs – which may, unfortunately, mean that the insurance industry could be the next one to start to see staff layoffs.

8. Pandemic Claims may Lead to Bankruptcies

P.J. Millar, Partner at Wallace & Turner Insurance

Being in the insurance industry (as an Independent Agency Owner), I’ve learned, or should I say had it reaffirmed, that while most commercial insurance buyers understood the fact that Pandemic/Virus “claims” are basically not covered, some see it as an attempt by insurance companies to not cover claims, “just because.” Technically, all property policies exclude (do not cover) such claims, and there’s not another source or method to buy the coverage. The same exclusionary language exists for flood, and yet flood is almost always available and usually reasonably priced; however, the number of flood policies purchased each year falls woefully short.

So, which calamity would you have bet on to wreak havoc in the U.S.? If you were offered Pandemic/Virus coverage last year, would you have laughed it off like being offered Volcano coverage?

While there aren’t many reports out yet to determine the dollar value of what would be considered covered Pandemic/Virus claims, most guesses are that it would have eclipsed the trillions that the Federal Government expended and would have caused widespread bankruptcies in the insurance industry.

The premiums currently and historically charged for property coverage contemplates known perils (fire, wind, etc.) and without calculating and charging for the potential expense of paying an excluded item such as Pandemic/Virus, it would cause the widespread, if not total devastation, in the insurance and financial markets.

9. Client Acquisition and Retention

Daniel Adams| CEG Life Insurance Services

As the owner of a small independent insurance agency, I feel the two biggest challenges in the insurance industry associated with COVID-19 are likely the same, or similar, challenges faced in other industries at this time as well-

- First, how to obtain new clients when people are unemployed, financially hurting, and looking to more immediate needs and benefits

- Second, with revenue decreasing as a result of business slowing down, how to retain and pay current employees.

However, as business slows, small business owners now have a great opportunity to spend time thinking, innovating, and planning for the future. COVID-19 will not keep business down forever, but it will change industries, consumer interests and desires, and how transactions occur. As a result, by spending time looking to the future through careful study, planning, and continuing to invest in their business, small business owners will be able to both survive the current circumstances and come out better as a result.

10. Absence of Physical Communication is making Everything Difficult

Garrett Ball, Owner of 65Medicare

My company works specifically with Medicare Supplement insurance plans. Because we serve the segment of the population that is, arguably, the most affected by the COVID-19 disruption, we have faced both major challenges and major opportunities as a result of the current crisis. The biggest challenges for us are the ability to meet with clients in a face-to-face setting – this has gone away for the time being due to the virus.

Everything we do has moved to online and phone meetings. Additionally, there are the psychological challenges of dealing with a population that is anxious about the potential contraction of the virus. We have fielded more phone calls than ever from clients concerned about the impact on them of this virus. At the same time, this has represented opportunity as more and more people in this age group are taking their needs seriously for optimal health insurance coverage and pursuing plans that limit their financial exposure to out of pocket costs should they need medical care due to the virus or other illnesses.

11. Multiple Challenges associated with Reopening

Elizabeth Schenk, AAI, CPIW, Chief Executive Officer | Agency Network Exchange, LLC

The impact of COVID-19, from an insurance perspective, is changing daily for business owners. There were a series of challenges over the last 8 weeks. The most current involves understanding their obligations to their employees and customers as they begin the phase of reopening.

The primary exposures are liability, worker’s compensation, and employment practices liability. The business owner must understand what measures they are required to take in order to protect the general public, how to address employees returning to work.

From a Worker’s Compensation and HR perspective, how does the employer deal with an employee who is afraid to return to work? What happens if an employee contracts COVID-19 during the course of their work? Has the business owner followed all safety rules?

12. Refining and Re-defining the Insurance Processes

Zhaneta Gechev, founder of One Stop Life Insurance

There is zero doubt that Covid-19 is changing every aspect of the world as we know it. It is changing the insurance industry as a whole.

Just about every insurance company is going remote. While this is just a small piece of the puzzle, it could have big ramifications. For example, Nationwide has announced that they consider continuing to have remote employees even after the pandemic is over. This could potentially leave many commercial buildings vacant.

In addition, life insurance carriers are revisiting their guidelines when approving coverage. As an agent, it is interesting to me to see how fast the industry is shifting. Most carriers we represent, have made adjustments to their underwriting, and have added additional Covid-19 questionnaires.

In addition, life insurance companies will be paying close attention to the illustrated rate of return on the illustration of their permanent insurance policies. Also, many of the traditional annuity seminars or informal dinners have been canceled and are replaced with virtual meetings and webinars. This is just a small sample of the metamorphose the industry is experiencing.

On the business insurance side, people will be paying close attention to their policies. Many policies do not provide interruption of business due to declared pandemic. Unfortunately, businesses forced to close were left with no help. As of now, I am not aware of any major shifts in the personal line insurance policies such as auto and homeowners insurance.

13. A Plethora of Internal and External Challenges to Deal With

Doug Groves, Principal | Program Insurance Group

Major challenges for business opening back up after COVID-19:

- Making sure customers are ready to visit your operation.

- Making sure your operation is safe and following CDC guidelines.

- Making sure your employees are safe and comfortable and trained.

- Patience with all.

- You are not going to rush customers, employees or suppliers, patience.

That is the way we are answering questions to clients around the country. Different kinds of businesses might have a few different concerns, and a visit with an insurance professional is always in order. We have stayed in touch with our clients and are wishing everyone to get open as soon as you can meet the above requirements.

Five types of insurance are critical through COVID-19 and in any crisis:

- Property Insurance

- Liability Insurance

- Employment Practices Liability Insurance

- Workers’ Compensation

- Automobile Insurance

14. Dealing with the Rising Cyber Threats

Jack Kudale, Founder & CEO of Cowbell Cyber

COVID-19 challenges for the insurance industry go beyond business interruption claims, with a rapid shift in the risks and exposures that cyber policies might have been designed to cover.

For example, businesses with work-from-home employees have a completely different cyber risk profile than what their security efforts might have prepared them for and face increased cyber exposure. Brick and mortar companies have started to transact online opening their business to cyber threats. Email scams related to COVID-19 are targeting relief operations.

One imperative for both policyholders and insurers is to review existing policies and evaluate whether they address the new threat landscape. This is also a good time to consider standalone cyber insurance options to get clarity over coverages, limits, as well as protection from new threats, including social engineering and ransomware.

15. Travel Insurance Claims have become Complex than Before

PK Rao, President of INF Visitor Insurance, INF Health Care

Travel Insurance has been particularly hit with COVID-19 claims. Not only from a trip cancellation standpoint- but a medical coverage standpoint as well! If you look at the market, most international companies have withdrawn or will withdraw Cancel for Any Reason Coverage, and moreover, you will probably see a do-away with $15 – $45 policies, which have become the norm.

The post-Covid-19 environment will see either rates rise, policy coverage more restrictive, or withdrawals itself from the market. INF stands by our members- providing travel medical coverage for Covid-19 sicknesses.

16. The Travel Industry is at the Receiving End during COVID-19 Crisis

Judith Segaloff | K2 Global Communications

Travel insurance can certainly claim a prime spot among the industries taking a particularly large hit due to the COVID-19 crisis. The Association of British Insurers (ABI) expects travel insurers to receive 400,000 COVID-19-related claims, resulting in £275 million in cancelation and disruption payments to customers – almost twice as much as the previous record of £148m back in 2010.

To date, more than 30 insurers have temporarily stopped selling travel insurance, and a further 19 have altered their policies to exclude coronavirus-related claims as well as future pandemics.

Yet the future might not be so bleak for insurance companies.

Firstly, we expect to see a general increase in appetite for travel insurance. We will be particularly wary of having our holiday plans canceled or of experiencing health problems abroad without appropriate medical coverage. Secondly, we anticipate seeing a significant change in the coverage offered by travel insurance.

Insurers should start using services, enabling sick or injured travelers to seek help from a network of qualified and vetted medical professionals. At Air Doctor, we tested this model with the Phoenix Insurance company, with stellar results. Overall, we observed a 30% increase in traveler’s health insurance revenues, coupled with a 14% reduction in medical visits claim costs. The numbers speak for themselves: integrating such services can be a game-changer for travel insurers.

COVID-19 brought the world of travel insurance on the edge of change. Time for insurers to adapt and thrive!

17. Retaining Customer Trust is becoming Tough

Christopher Liew, Founder of the Wealth Awesome

Being an owner of an insurance brokerage company, I’ve had discussions with many companies. Based on that, here’s my assessment of the challenge the sector is facing: Lack of Trust.

This is a big reason why many people are hesitant about entrusting insurance companies with hard-earned money. This lack of trust can be attributed to the malpractices of some corrupt insurance firms that fail to pay claims to their customers, besides not being transparent in disclosing the benefits and offers they can leverage.

Some people even classify insurance companies as a financial burden. Owing to these challenges, many insurance firms have had to shut down. The customers

who have suffered losses at the hands of such players are reluctant to purchase insurance policies again in their life.

To overcome this challenge and inspire trust among their potential customers, insurance companies are now focusing on consistent communication via different channels such as social media, emails, and text messages.

18. Delayed Insurance Coverage Purchases due to Social Distancing

James Pollard | The Advisor Coach LLC

One of the biggest changes is that a lot of people don’t want to have a nurse come into their home to give them a medical exam. Thus, a lot of people are either delaying insurance purchases or opting for insurance without a medical exam, which can be significantly more expensive.

Other than that, insurance agents have been doing a lot more virtual work. Some love it, and some hate it, but I’m confident that the industry will adapt over time.

19. Rising COVID-19 Claims and Complex Documentation are Leading to Errors

Alexander Balladares, Operations Director at Marketheir

We are seeing an alarming number of business insurance claims being filed from local business owners negatively affected by COVID-19. In major metropolitan cities such as Los Angeles, there are thousands of these claims that are being immediately denied by insurance companies due to the misreading of policy terms by their adjusters.

There are more than 6,000 insurance companies currently dealing with the economic fallout of COVID-19. A typical insurance policy is anywhere between 550-600 pages. With highly complex documentation like this, it’s common for these claims to be wrongfully denied, leaving business owners at a major loss and at risk of even further damages. One of the most vital pieces of our society is being left out to dry when they need assistance now more than ever, as they are forced to either accept the loss or take up the fight in court.

Conclusion

Well, this clearly lets us know that it is not just one challenge but multiple challenges in the form of rising claims, technology adoption, increasing customer queries, etc., that the insurers are facing in the present COVID-19 scenario. Every insurer is trying its best to quickly adapt to digitalization and make the best use of available resources to retain and acquire clients.

However, a lot of processes, especially the back-office ones, are making things complicated for insurers owing to a lack of staff, expertise in using technology, and more. So, what should insurers do about this? The best way to deal with this challenge is to collaborate with one of the top insurance outsourcing companies. This will help insurers in freeing themselves from back-office management chores and instead focus on prime tasks.

Meet Insurance Support World, a renowned insurance outsourcing services provider worldwide providing quality back-office support to firms for more than 12 years. Start a free trial by getting in touch today itself!

Recommended Posts:

Tips for Insurance Firms to Improve Claims Management Process

Opting Commissions Management Services – Consider Key Factors

An Insight to Outsourcing Policy Management Services

Outsourcing & Insourcing: A Healthier Mixture for Insurance Claims Management

Businesses face mounting pressure to decide between in-house, outsourcing, or hybrid models. The insurance sector is no exception. For insurance claims management, the line between insourcing and outsourcing blurs. If an organization has a robust in-house team, outsourcing may not be necessary for better quality and cost-effectiveness.

In the claims dome, countless processes can be handled in a number of ways. Some insurers who handle the claims process internally got good results, and some got great opportunities. However, other insurers prefer outsourcing services for their end-to-end process, and you may find modifications in results. Looking at the variety of approaches, it seems the best result will occur when insurers embrace the “all of the above” approach.

By analyzing both internal proficiencies with external niche skills, insurers with the craving for an innovative end-to-end insurance claims management services are likely to see both- high quality and best endings.

Benefits that can be reaped from this type of multi-channel insurance claims management approach:

Reduced operational cost-

From the traditional viewpoint, outsourcing often meant employing business partners out of the country as an approach for manufacturers to reduce costs while refining quality. But today, much of the outsourcing companies are in the US, especially as it relates to the insurance claims processing.

For instance, an insurance company in Montana receives five claims per month. So what you think, does it put some logic to staff in-house team from different geographic regions with poor results? Is it not a smarter way to gain benefits of hiring an independent assistant in your geographic area, enabling you to focus on your internal staff with higher claims counts? By utilizing an appropriate external team, insurers can radically reduce their overall expenses.

Improved efficiencies-

See every business wants steadiness, and efficient processes and insurance business is not an exception in this regards. More so, claims management is one of the important operations for insurers as it entirely impacts the reputation of the company. Now you think for a while, your in-house adjusters seriously have this much time to analyze each medical bill or review a CPT coding manual for future services? It’s obviously no! Therefore, hiring an external claims team who can precisely look after each document can help your adjusters to settle claims faster, which ultimately increases your client satisfaction ratio.

What happens next? You’ll observe efficiency throughout your claims lifecycle as identifying productiveness is the excellent component to the long-term success of your insurance carrier. There will be a tremendous improvement in the overall productivity of your in-house team and adjusters.

Domain experts-

Typically, the most challenging job for every insurer or any other business owner is finding niche expertise. Possibly, the chances are higher in the insurance industry as for claims processing they have seen an aging workforce retiring faster than being substituted. This is actually threatening the insurers as many organizations are moving towards new business models that emphasize on productivity at the cost of necessary claims competency.

Well, you can attain this business model by embracing the outsourcing model. How? Outsourcing firms have skilled and experienced niche expertise that deliver quality and accurate insurance claims management services, freeing up the insurer’s time so that they can focus on what they do best!

For example, subrogation cases are where claims have a hard time. With the help of the external skilled team, insurers can easily uplift their recoveries rate while reducing expenses.

Growing technology-

According to researchers, there are three key routes to success- processes, people and technology. Don’t get confused with technology because many entrepreneurs think that embracing new tools is the only solution. However, technology is used as a crucial tool to enhance both people and processes efficiently. In case of basic claims investigation, technology can help claim adjusters in making viable decisions about coverage and outstanding amount. Technology also addresses the common issues that include inadequate understanding of the concept of liability, stop you from taking shortcuts and help you negotiate on fundamentals.

Enhanced management-

Once your insurance claims management process gets streamlined, being an insurer, you can stay focused on your core competencies that include encouraging underwriters, policy management, tracking commissions, etc. This eventually impacts the management of the insurance carriers as they can focus on formulating new policies for the sake of business growth.

Bottom Line

Making the right decision can be daunting; however, above-mentioned benefits may help you up to a certain extent. Try to define your business goals and evaluate the need for insourcing and outsourcing insurance back-office services with your team.

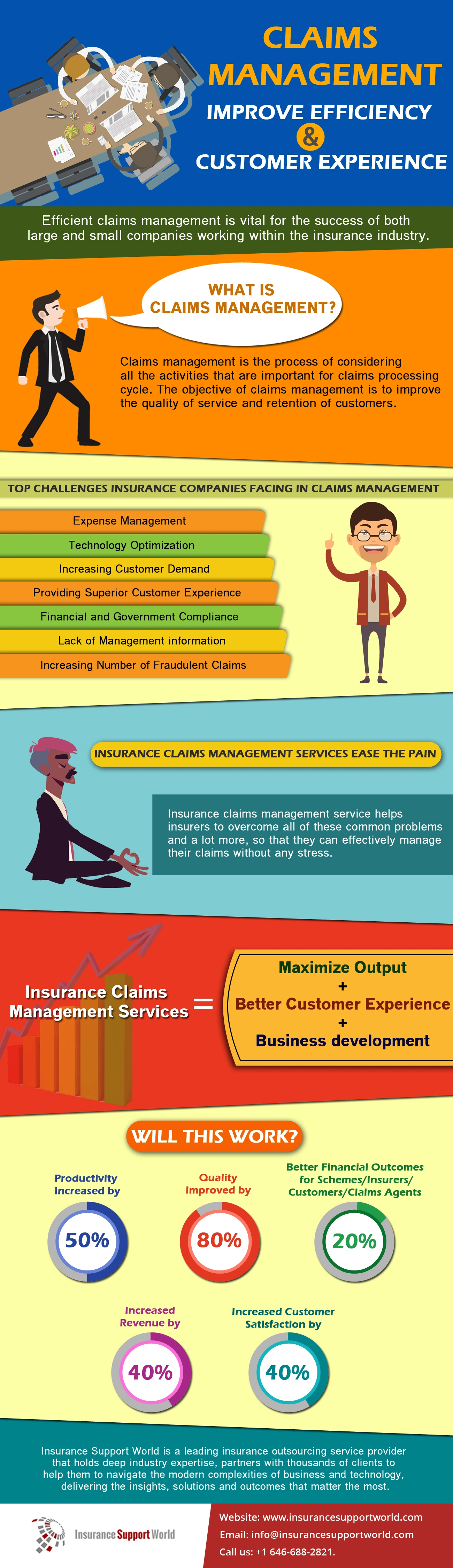

Insurance Claims Management : Improve Efficiency and Customer Experience

Insurance claims management is a crucial task in the Insurance Industry. It is complicated, but the profit is based on this aspect as customer satisfaction is the most important part here. Settling Insurance claims efficiently is not an easy task, it should be particularly focused and minute calculations are required. So there’s an intense need for the Insurance industry to bring improvement in their work efficiency to retain the customers. Regardless of business size, it is necessary for insurers to handle the insurance claims management services appropriately. This will generate huge profits and increase overall business growth.

Efficient insurance claims management is the cornerstone of a successful insurance business. It offers the potential for both improved operational efficiency and enhanced customer experiences. The key to achieving this lies in reducing processing times, which can be significantly expedited through modernizing claims processes. How? Leveraging technology and automation. A streamlined approach not only benefits the insurance provider by expediting claims processing but also ensures that policyholders gain faster access to necessary funds or services. Furthermore, embracing automation and digitization improves claims processing accuracy, reducing the likelihood of human errors and ultimately fostering greater customer satisfaction and trust in the insurance provider.

Effective communication is another essential component of handling claims. Policyholders need to be informed at every stage of the process, from initial claim submission to resolution. This transparent approach builds trust and keeps customers engaged and informed, even during potentially stressful claims processes.

Additionally, the use of data analytics can identify potential fraudulent claims, protecting the insurer’s financial interests and maintaining competitive premiums for honest policyholders. It also ensures that the claims process remains fair, efficient, and customer-centric.

How Insurance Claims Management Improves Efficiency

Tips for Insurance Firms to Improve Claims Management Process

Seeking to improve the insurance claim management process, through an elaborate effort, is what you should be going for if you’re running an insurance claim business. Not only will run your business more efficiently, but you will also reap the benefits of favorable financial changes and improved customer relationships. The claiming process for each claim has a different process attached to it; however, you can perform certain facets in a standard method. Refining the methodology that goes into the claiming process and using technology wisely can raise the bar for this standard.

You should definitely look at your competitors for ideas on what to do and what not to do, but following them blindly is something that you should avoid. Your organization, just like every other one, has its own strengths and weaknesses and these should influence the way you refine your methodology in claim processing. Let us look at some proposals which can aid you in this matter.

Understand the aspects affecting the claim management process-

Just like every industry, even the insurance sector is undergoing tremendous change to transform their operations and become more streamlined. Furthermore, the claims management process generates chunks of data on a daily basis, which ultimately requires accurate processing to provide quality services to customers, ensure more precise calculations, and maintain continuous efficiency in the insurance claims management process.

However, relying entirely on insurance claims system will take you nowhere as they cannot deal with millions of data efficiently. A transformed claim management process require appropriate use of the technology, dealing with cost pressure, staying compliant with regulations, and much more.

Master the Data and Technology Management-

Interconnecting the network that a business stands upon is essential. Isolated systems will cause slowdowns and decrease the efficiency of claim processing. Be smart, and upgrade your technology to what is latest in the market. Efficient tools that allow you to analyze data and perform predictive modeling will help you in your endeavor. You will not only find more opportunities for growth but also set yourself apart from your competition. Improved customer service will help you retain customers and earn their loyalty.

Top Notch Customer Service

If anyone’s ever had to file an insurance claim, it’s probably due to a very stressful reason. They definitely want to streamline the whole process in a very satisfactory manner. As an insurance organization, you would want to fulfill this. Consistent service in all forms of communication – be it via the phone, e-mail, Skype, face-to-face live chat – will help you win your customers heart. Each new claim that comes in is a chance to gain a new loyal customer; your organization being able to satisfy and retain customers will make your business more successful.

Comply With the Regulations

If you’re in the insurance claims management business, you’ll know there are a lot of regulations set upon your organization. They must all be very carefully adhered to. One misstep and the whole process go awry. Make sure the insurance claims processing systems that are involved in the process aren’t isolated. Any inefficient processes that are manually intensive will greatly hamper the whole process and increase the risk of a fault and cost you a fine or penalty! Your methods should also be completely transparent to the customer. And being able to show that you adhere to regulations consistently will help sail smoothly.

Invest in ‘Smart’ Technology

Smartphones these days can do a lot of things. You have the option to invest in the development of an app. This app can provide your customers with easy access to your claims services through their smartphones. Additionally, you can acquire an app designed for your claims adjusters. This app will enable them to access data from any location, facilitating faster claims settlement.

Conclusion

The efforts you put into your endeavor of providing the smoothest, most satisfactory claims management services to your customers will ensure your reputation in the market. The higher your efficiency, the higher the customer satisfaction and the more loyal customers you’ll get. Eliminate the manual tasks and automate as many functions as you can to reduce the chances of errors. Make sure your network is working properly so that data can go across departments with ease. Follow the tips mentioned above, and you’ll definitely achieve higher levels of efficiency in your insurance claims processing business.

If you are looking for insurance back office outsourcing, get in touch with Insurance Support World today. Our contact number is +1 646-688-2821 and the email ID is info@insurancesupportworld.com.

Insurance Claims Management : Is Outsourcing Right Step?

Insurance claims management is an important process in insurance firms. It helps in settling claims, detecting fraud, avoiding the necessity for litigation, etc. Insurance companies are facing a lot of competition from their rivals. They are trying their best to reduce their operational costs. In such a scenario, hiring insurance claims management outsourcing services can prove to be a great option for insurance firms looking to concentrate on their core tasks.

Advantages of Opting for Insurance Claims Management Outsourcing Services:

Access to a variety of services – The outsourcing firms offer a variety of services like first notice of loss management services, claims verification, and validation, claims processing services, claims adjudication services, subrogation, maturities processing, early retirement, withdrawals, reconciliations, file closure, and portfolio management etc.

Ensures proper handling of claims process management – Outsourcing firms will ensure customer satisfaction by settling the claims correctly, with no wrong claims. It will ensure that the clients don’t have to pay additional premiums as the costs incurred by the insurance firms would be lesser.

Access to proficient staff – The outsourcing insurance claims management firms are well known for having access to highly qualified staff that can recognize the false claims and ensure correct settlements in a prompt manner. So without actually hiring anyone you can enjoy the services of proficient staff. This can help save a lot of time that would have been spent in recruitment, overseeing, training, etc.

Helpful during times of urgent need – There are situations where the insurance companies require urgent claims management services. In such a scenario the third party outsources claims management firms are the best option. With their round the clock operations, they can offer quick results and help in cases of urgent requirement.

Economical in terms of cost – Outsourcing services are generally more affordable. Most of these firms have their offices in developing nations like India, South Africa, etc. In these countries, the remuneration charges are much less. Moreover outsourcing also helps in eliminating the payroll and infrastructure costs.

Offer the opportunity to concentrate on productive activities – By outsourcing the claims management services, an insurance firm can concentrate on important functions like marketing and customer relationship management and maximize their revenue. Moreover, by eliminating the false claims of unscrupulous clients, an insurance firm can reduce their losses.

Assured privacy – Outsourcing firms maintain 100% privacy and ensure the safety of a firm’s documents from unnecessary intrusion.

The above-mentioned information can encourage the higher management of an insurance firm to hire outsourcing insurance claims management services.

Bottom Line

Insurance Support World has emerged as a successful provider of outsourcing services to insurance companies from all over the world. Since 8 years, it has created a niche for itself in this field and earned the goodwill of clients. These services can help insurance firms maximize their potential, sustaining their profitability and gaining an edge over competitors. To get more information, contact us at info@insurancesupportworld.com or call us at +16466882821.

Benefits from Claims Management for Insurance Sector

In the present competitive business environment insurance companies are facing a variety of challenges. The ever-changing government regulations and the enhanced expectations from clients are keeping the insurance companies on their toes. Following the right insurance claims management strategy is one of the ways of enhancing the efficiency of insurance firms. This can help in reducing costs and eliminating frauds while ensuring the happiness of clients.

Benefits of insurance claims management:

Aids in settling Claims – The basic purpose of claims management is to check the merit of a claim and make a correct assessment of how much a client deserves. If the claims are settled as per customer satisfaction, then the goodwill of the company increases.

Helps in detecting frauds – By ensuring that there are no frivolous claims, this process helps in reducing losses. It also helps in keeping the insurance premiums paid by consumers to a lesser amount, thus keeping clients happy.

Helps in avoiding unnecessary costs like litigation – A professionally followed claims management process can help in eliminating additional costs like litigation for an insurance company.

Insurance claims management outsourcing is an ideal solution which can help in completing them quickly and effectively. The outsourcing firms are capable of processing a large volume of claims for while keeping the guidelines in mind.

Generally, the outsourcing firms follow the following processes during insurance claims management:

- Damage assessment

- Documentation

- Successive claims submissions

The outsourcing firms have access to proficient staff fully capable of recognizing the false claims and ensuring faster and right settlements. The third-party firms are also capable of offering round the clock operations in cases of urgent requirement. With their result oriented and proven strategies, an insurance company is bound to reap the benefits.

The outsourcing insurance claims management services offered by third-party firms include accessing the relevant documents on a remote server through a virtual network, evaluating the legitimacy of claims, determining the exact due amount, etc.

Benefits of outsourcing insurance claims processes:

- The outsourcing services are considered more economical as they are based in nations like India, where service charges are cheaper than the cost of spending on payroll and infrastructure in developed nations.

- These services enhance the productivity of the insurance firms by eliminating false claims and allowing them to concentrate on marketing and customer relationship management, thus optimizing their revenue.

- The outsourcing firms maintain 100% privacy and ensure the safety of a firm’s documents from unnecessary intrusion.

The above-mentioned information can encourage the higher management of an insurance firm to hire outsourcing insurance claims management services.

Insurance Support World has emerged as a successful provider of outsourcing services to insurance companies from all over the world. In the last eight years, it has created a niche for itself in this field. These services can help the insurance firms in maximizing their potential, sustaining their profitability and gaining an edge over competitors. To get more information, contact us at Email info@insurancesupportworld.com or call us at +16466882821.

Importance of Outsourcing Insurance Claims processing

Efficient handling of insurance claims is a cornerstone for insurers. Outsourcing this process has become a strategic move for insurance companies. It helps to streamline workflows, reduce operational costs, and improve customer satisfaction. Let’s dive into the benefits of outsourcing insurance claims processing. and how it simplifies processes

Benefits of outsourcing insurance claims processing

-

Time to focus on primary business activities – Claims processing is a back office task. It does not fall under the ambit of core activities. It primarily consists of selling policies and structuring new schemes to offer a range of alternatives to customers. Claims arise often decades after you sell a policy. Hence there is no point in tying up huge investments for maintenance of old accounts. Outsourcing this function results in reclaiming the time you have for business growth and development.

-

An increase in total productivity – Productivity is an indicator of a company’s ability to get the best out of employees. It ideally one of the top measurable performance parameters. These mainly rest on total sales in the current year and the incremental business over last year. Reaching business targets is another criterion. It is crucial to divert trained and qualified manpower from the claim processing tasks. This will further allow them to focus on increasing sales and enhancing productivity.

-

An increase in market share – This is not a direct impact of the decision to outsource insurance claims processing but is nevertheless crucial. By outsourcing, there is no need to invest heavily in infrastructure, state of the art hardware and software and trained personnel. Use this capital savings to structure policies and schemes with highly competitive prices. With the support of dedicated insurance retailers and wholesalers this pricing strategy increases market share.

How Claims Processing Streamlines the Process

-

Quick claim eligibility evaluation – Top claims outsourcing agencies have the required systems in place to deal with claims processing. The complexity of it is visible by the fact that placing a claim after the lapse of a very long period from the purchase of the policy. Verifying old records meticulously especially the history of premium paid before sanctioning a claim is itself a daunting task, multiply that by the hundreds of claims presented for payment every month and the true magnitude comes to the fore. Just outsourcing this one task guarantees a huge load off your shoulders freeing you up for more productive activities.

-

Quick settlement of claims – There is no doubt that the reliability and integrity of an insurance company depend on the speed of settlement of claims. This is the promise that was in-built and obvious when the policy was sold and any deviation can impact the credibility of the company and impede business growth and development. By deciding to outsource insurance claims processing this aspect is fully covered. These agencies have skilled and trained resources that can quickly trace back to old records, verify their genuineness, evaluate the legitimacy of the claimants, process the claims and facilitate quick disbursal. An insurance company will not have any stake in this – the whole process will be comprehensively taken care of. Just imagine the load it would otherwise put on the insurance company.

-

Accuracy in claim disbursal – After the claim is settled experts and auditors carry out a thorough due –diligence check to make sure that the amount paid is correct in all respects and that disbursal has been made to the actual claimant. The insurance company thereby is not put at a loss and is also insulated from any future litigation.

Choose ISW as your Strategic Outsourcing Partner

These are some of the reasons why outsourcing of insurance claims management services is so important in the insurance sector today.